The Rise of Portable Benefits

A once-niche idea is quickly becoming a nationwide movement to expand benefits without sacrificing flexibility.

Seven years ago, I wrote a research paper that I later developed into a policy framework establishing a safe harbor for voluntary portable benefits for independent workers—clarifying that benefits can be offered without triggering reclassification risk.

When I first started talking to policymakers in February 2020 about portable benefits, the idea was still largely theoretical—something that lived mostly in research papers and policy conversations, not in actual law.

Over the years, I’ve testified before Congress and in state legislatures across the country on this issue, and my conversations with policymakers consistently reflect a genuine interest in addressing this gap.

Today, that idea has moved firmly into the mainstream.

In the past three years, 18 states have introduced, enacted, or piloted portable benefits reforms—turning what began as a single-state effort into a rapidly expanding, multi-state policy movement. At the same time, two major congressional bills are advancing similar safe harbor frameworks at the federal level.

As more states adopt these frameworks, portable benefits are quickly moving from a policy experiment to a central part of the national labor policy debate.

The Map: A Policy Movement in Real Time

What’s striking is not just where portable benefits are appearing—but how fast.

States like Alabama, Idaho, Tennessee, Utah, West Virginia, and Wyoming have already enacted voluntary portable benefits frameworks. Others—including Pennsylvania, Maryland, and Georgia—have launched pilot programs. And a growing number of states—from Connecticut to Kansas to Hawaii—are actively considering legislation. Below is a list of state-level portable benefits legislation introduced in 2026:

Connecticut — H.B. 5041 (health care benefits)

Florida — H.B. 1431

Georgia — H.B. 987

Hawaii — S.B. 2088 (health care benefits)

Kansas — H.B.2602 (includes tax advantage)

Kentucky — H.B. 732

Louisiana — H.B. 301

Mississippi — H.B. 1072

New Hampshire — H.B. 1245

Rhode Island — H.B. 7365

This kind of policy diffusion is rare. It signals something important: lawmakers across very different political and economic environments are converging on the same idea.

This momentum has been supported by a growing coalition of policy organizations, researchers, worker advocates, and industry stakeholders working to expand access to portable benefits.

What Portable Benefits Actually Do

At their core, portable benefits solve a simple but deeply embedded problem in U.S. labor policy.

Our benefits system was built around a single-employer model. But today, roughly 30 million Americans work independently, generating nearly $1.5 trillion in economic activity annually.

The independent workforce has grown by 97 percent since the late 1990s.

And yet, many of these workers lack access to benefits—not because companies are unwilling to offer them, but because the law makes it risky to do so.

Portable benefits directly address this problem. They are worker-owned accounts that follow individuals across jobs and allow multiple companies or clients to contribute. The key policy change is simple: remove the legal risk that offering benefits will trigger worker reclassification.

Under current law, the presence of benefits can be used as evidence that a worker is an employee. Portable benefits laws clarify that this should not be the case.

In other words, voluntary portable benefits safe harbor reforms don’t mandate benefits—they make it possible to offer them. By contrast, other portable benefits bills are typically mandatory or limited to app-based industries.1

Three Reasons This Is Taking Off Now

There are several reasons this momentum is accelerating.

First, the workforce has already changed. Independent work is no longer niche—it now spans industries ranging from professional services and healthcare to transportation and the arts. Surveys increasingly show that Gen Z is more interested in self-employment and entrepreneurial work than previous generations at the same age—a shift that is already shaping how policymakers think about the future of work. This approach has also been supported by state policymakers, including through a 2023 framework developed by the National Conference of State Legislatures.

Second, workers themselves are asking for it. About 80 percent of independent workers prefer to remain independent, and roughly 81 percent say they want access to portable benefits.

Third—and most importantly—this approach breaks a long-standing policy stalemate.

For years, the debate has been framed as a binary choice: either force workers into traditional employment or leave them without benefits.

Portable benefits offer a third path: expanding access to benefits while preserving flexibility.

Are There Downsides? Addressing the Biggest Concerns

As portable benefits spread, a predictable set of questions comes up. These are worth addressing directly.

1). Does this increase misclassification?

No.

Portable benefits policies do not change the legal definition of employment. They do not alter existing classification tests—whether it’s the ABC test or common law standards.

They simply clarify one narrow point: the presence of benefits cannot be used as evidence of employee status.

For example, states like Connecticut, which already use one of the strictest worker classification tests in the country (the ABC test), can adopt portable benefits without changing how that test is applied.

This is not about redefining work—it’s about removing a barrier that prevents benefits from reaching workers who are already independent.

2). Why not just make everyone employees?

Because most independent workers don’t want that.

Independent work provides autonomy and flexibility that traditional employment often cannot—especially for caregivers, parents, students, and those managing multiple income streams.

Portable benefits meet workers where they are. They expand access to benefits without requiring workers to give up the arrangements they prefer.

In states that have taken far more restrictive approaches, the results have often backfired. In California, for example, AB5 had to be partially rolled back with over 100 occupational exemptions. Our research shows that for occupations that were not exempt, independent work declined without any corresponding increase in W-2 employment.

3). Will companies actually contribute?

Yes—and we’re already seeing it happen.

Once the legal barrier is removed, companies begin to participate. Portable benefits programs in multiple states show that businesses are willing to contribute when they have clarity and certainty.

As an example, in Pennsylvania, workers in the DoorDash pilot program received more than $1.3 million in benefits. Nearly 75 percent of workers who previously lacked access to benefits gained access through a portable benefits program. Among them, 81 percent reported feeling more financially secure, and 95 percent said they would feel even more secure if the program were made permanent.

The demand is there—from both workers and companies. The missing piece has simply been legal clarity.

What Does the Data Actually Show?

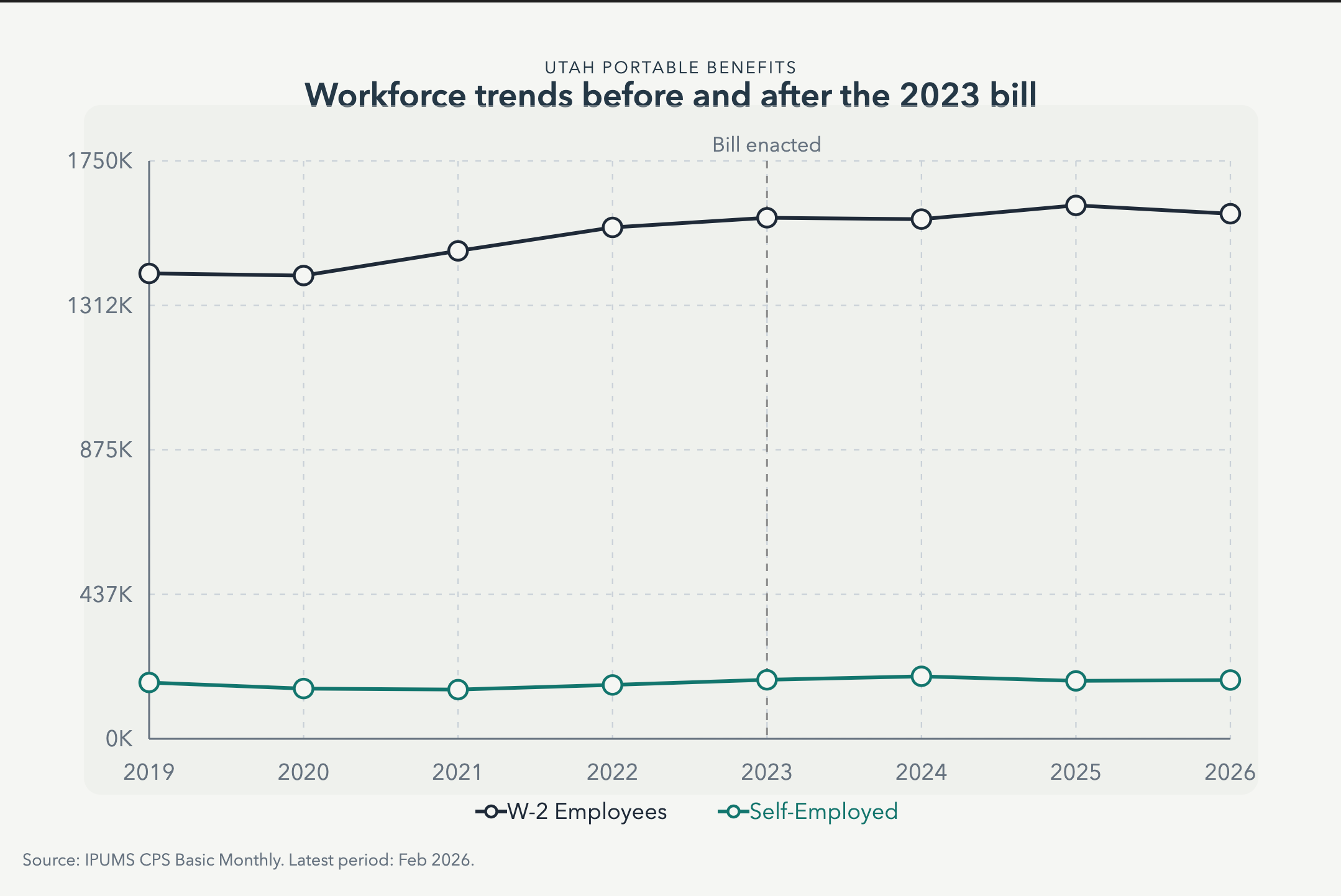

The best real-world evidence so far comes from Utah—the first state to adopt a voluntary portable benefits framework.

My research team analyzed outcomes in Utah, where a portable benefits policy took effect in 2023. The early evidence shows that traditional W-2 employment and self-employment continued to grow at similar rates as before. The policy simply allowed independent workers to access benefits.

In essence, W-2 employment growth remained stable after the bill’s enactment. Self-employment continued its steady growth pattern unchanged. There was no disruption to overall labor market composition.

This reinforces a broader point: independent work and traditional employment are not in conflict—they coexist and often complement one another. Most workers still rely on W-2 employment, while many also engage in independent work as a supplement or alternative depending on their needs.

Portable benefits fit within that reality.

They are complementing, not replacing, traditional employment—expanding access to benefits without reshaping or undermining the existing labor market.

What This Means

Taken together, these developments point to something bigger than a single policy reform.

We’re watching the early stages of a structural shift. States are experimenting and codifying portable benefits frameworks in real time, pilot programs are demonstrating proof of concept, and federal policymakers are beginning to take notice. If the past three years were about state-level innovation, the next phase is likely national—where a federal safe harbor could allow these models to scale across industries and states.

But even without federal action, the direction is clear.

Portable benefits are no longer a niche idea—they are becoming a standard part of modern labor policy.

For decades, the U.S. benefits system forced a tradeoff: flexibility or security. Portable benefits are beginning to break that tradeoff.

And what’s most striking isn’t just the idea itself—it’s the speed at which it’s spreading. What started as a fringe concept is now moving state by state, law by law, into the mainstream of American labor policy.

This voluntary portable benefits model differs from other approaches—such as those in California (Prop 22), Washington, and Massachusetts—which require companies like Uber, Lyft, DoorDash, and Instacart to provide a defined set of benefits to gig workers.

The portable benefits movement is a genuine improvement and the state-level momentum is real. But it's worth naming what it is: a workaround for a structurally broken system rather than a fix to the structure itself.

The reason 30 million independent workers lack benefits isn't primarily a legal classification problem — it's that benefits are tied to employment at all. The 1954 tax code decision that made employer-sponsored benefits tax-exempt created the entire architecture that portable benefits are now trying to patch. Workers are still dependent on someone — employer or client — contributing to their account. Coverage still isn't truly universal.

The deeper fix is severing the link between employment and coverage entirely. Coverage that follows the person regardless of employment status — W-2, 1099, sole proprietor, caregiver, between jobs — doesn't need a portable benefits framework because it was never attached to a job in the first place.

That's the architecture the Burned at Both Ends — B@BE — framework is built around. burnedatbothends.org — genuinely curious whether you see portable benefits as a bridge to that structural fix or as a destination in itself.

Companies want to offer benefits and workers want to receive them, but the legal structure keeps them apart. There is demand, but the real challenge is figuring out how to build the right market. The DoorDash pilot shows that when you remove the barrier, it works! Those numbers are convincing. Expanding to 18 states in three years is impressive progress. Great write up, Liya.